One of the biggest student loan myths out there is that borrowers can’t combine federal student loans and private student loans into one refinanced loan.

It’s understandable why people may think that, since this wasn’t always an option. And consolidation through the Department of Education is only available for federal student loans.

But now you can choose to combine federal and private loans. So it’s important to understand whether combining federal student loans and private student loans is right for you.

Can I Consolidate Federal and Private Student Loans?

Yes, you can combine private and federal student loans by refinancing them with a private lender.

Through this process, you actually apply for a new loan (which is used to pay off your original loans) and obtain one with a new — ideally lower — interest rate.

Why would you want to do this? In addition to the advantages of loan consolidation (like having one, simplified monthly payment), refinancing student loans at a lower interest rate may lead to lower monthly payments. Note: You may pay more interest over the life of the loan if you refinance with an extended term.

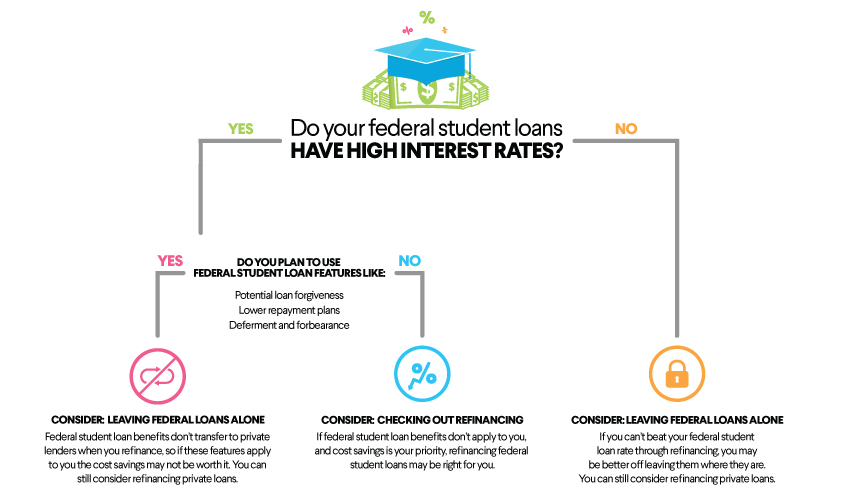

Before you refinance federal student loans, there are a couple of things to think about. Here’s an easy decision tree to help you understand whether private student loan consolidation and refinancing federal loans is right for you:

Federal Student Loan Interest Rates

Some people assume that federal loans always offer the best rates, but this isn’t necessarily true.

Depending on loan type and disbursement date, new federal student loan interest rates are reassessed annually, every July. For the 2023-2024 school year, interest rates on new federal student loans range from 5.50% to 8.05% . Interest rates on federal student loans are determined by Congress and are fixed for the life of the loan.

Some borrowers — particularly those with established credit and a strong, stable income or who can find a cosigner with similar qualities — may be able to qualify for a private student loan with a rate lower than a federal loan. For example, grad school borrowers who have higher-interest-rate unsubsidized federal Direct Loans and borrowers with federal Direct PLUS loans may also be able to qualify for a private loan with a lower interest rate than those federal loans. Undergraduates are likely to find lower rates with federal student loans — without a cosigner or credit check.

When you apply to refinance, private lenders evaluate things like your credit history and credit score, in addition to other personal financial factors, in order to determine the interest rate and terms you may qualify for. This applies when you consolidate private student loans as well.

This means if you’ve been able to build credit during your time as a student, or your income has significantly improved, you may be able to qualify for a more competitive interest rate with a private lender when you refinance. (If you aren’t interested in or don’t qualify for student loan refinancing, a Direct Consolidation Loan from the Department of Education might be worth a look — but you can’t combine federal and private loans into a Direct Consolidation Loan.) Private student loan consolidation is a different matter.

To get an idea of how much refinancing could potentially reduce the cost of interest on your loans, take a look at SoFi’s student loan refinancing calculator.

Federal Student Loan Benefits

When you refinance a federal student loan with a private lender, it becomes a private student loan. This means that the loan will no longer be eligible for federal benefits and protections.

Before you contemplate the idea of refinancing, consider taking a look at your loans to see if any of these federal loan benefits and programs apply to you — or whether you might want to take advantage of them in the future. Here are some to consider:

Student Loan Forgiveness

There are a few forgiveness programs available for borrowers with federal student loans. For example, under the Public Service Loan Forgiveness Program (PSLF), your Direct Loan balance may be eligible for forgiveness after 120 qualifying, on-time payments if you’ve worked for an eligible public sector entity that entire time.

Pursuing PSLF can require close attention to detail to ensure your loan payments and employer qualify for the program. The qualification requirements are clearly stated on the PSLF section of the Federal Student Aid website .

Similarly, the Teacher Loan Forgiveness Program is available for teachers who work in eligible schools that serve low-income families full time for five consecutive years. The total amount forgiven will depend on factors like the eligible borrower’s role and the subject they teach. The Federal Student Aid website has all the details of this program.

These forgiveness programs can be beneficial for people who choose careers in public service or education.

Income-Driven Repayment Plans

There are also a number of federal loan repayment plans that can ease the burden for eligible borrowers who feel their loan payments are higher than they can afford.

Under the student loan repayment plans and the other income-driven repayment options, monthly payments are calculated based on a certain percentage of the borrower’s discretionary income.

President Joe Biden’s Save on a Valuable Education (SAVE) Plan provides the lowest monthly payments of any IDR plan available to nearly all student borrowers.

But if your income is over a certain threshold, you likely won’t benefit from these programs.

And if you do qualify but you’re at the high end of the spectrum, your slightly lowered payments may come at a disproportionate price in the form of accumulating interest. Although the Department of Education says that if you make your monthly payment under the SAVE plan, your loan balance won’t grow due to unpaid interest.

Deferment or Forbearance

Life can be unpredictable — sometimes that means borrowers might have difficulty making payments on their student loans. When this happens, borrowers with federal student loans may qualify for deferment or forbearance.

President Biden proposed a federal student loan debt canceling of up to $20,000 for qualified loan holders but it was struck down by the Supreme Court in a ruling released in late June 2023.

The three-year-long pause on federal student loan payments due to Covid-19 lockdowns ends in the Fall of 2023. Student loan interest will resume starting on Sept. 1, 2023, and payments will be due starting in October.

For borrowers who can’t make payments, the DOE created a temporary on-ramp period through Sept. 30, 2024. This on-ramp period protects borrowers from having a delinquency reported to credit reporting agencies. And it prevents the worst consequences of missed, late, or partial payments.However, payments are still due, and interest will continue to accrue.

Also, there are ongoing deferment and forbearance options that allow borrowers to temporarily pause payments on their federal student loans in the event of economic hardship.

The biggest difference between the two is that with forbearance, the borrower is responsible for paying the interest that accrues on the loan during this time. Forbearance can have a major financial impact on a borrower, as any unpaid interest will be added to the original loan balance. With deferment, the borrower may or may not be responsible for paying the interest that accrues.

The type of loan you hold will determine whether or not you qualify for deferment or forbearance. Both options can be potentially helpful tools to borrowers going through a short period of financial difficulty, but both have important considerations .

Refinancing Your Student Loans

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

SoFi Student Loan Refinance

If you are a federal student loan borrower, you should consider all of your repayment opportunities including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. Please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans or extended repayment plans.

SoFi Private Student Loans

Please borrow responsibly. SoFi Private Student Loans are not a substitute for federal loans, grants, and work-study programs. You should exhaust all your federal student aid options before you consider any private loans, including ours. Read our FAQs. SoFi Private Student Loans are subject to program terms and restrictions, and applicants must meet SoFi’s eligibility and underwriting requirements. See SoFi.com/eligibility-criteria for more information. To view payment examples, click here. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOSL0723009